WIP Accounting for Construction: A Strategic How-To Guide for Profit Protection

- Wendy Okie

- May 20

- 12 min read

What if the project that looks most profitable on your ledger is actually the primary reason your bank account feels empty? Many contractors operate in a state of perpetual uncertainty. They see high revenue figures but struggle with inconsistent cash flow and financials that make securing larger bonds nearly impossible. It's a common frustration to only discover the true health of a project once the job is 100% complete, leaving no room for strategic adjustments. This guide will show you how to master WIP accounting for construction to eliminate these financial blind spots and stabilize your operations.

By moving beyond basic administrative tasks and building a comprehensive structural framework, you can transform your reporting from a backward-looking chore into a forward-looking early warning system. You'll learn how to identify over-billings and under-billings with precision; this ensures your profit margins remain predictable even as material costs for electrical gear and HVAC equipment rise by 8-10% in 2026. We'll explore the mechanics of contract assets and liabilities to help you produce lender-ready financial statements that reflect the true strength and stability of your business.

Key Takeaways

Understand how to move beyond the "profit illusions" of cash-basis accounting to gain a true picture of your project's financial health.

Master the mechanics of identifying over-billings and under-billings to ensure your cash flow remains stable throughout the project lifecycle.

Follow a disciplined roadmap for implementing WIP accounting for construction, including essential updates to your chart of accounts and monthly data reconciliation.

Learn how to leverage high-level financial reporting and controller-level oversight to strengthen your bonding capacity and secure larger, more profitable contracts.

What is WIP Accounting and Why Does it Matter in 2026?

In the construction industry, your bank balance is often a poor indicator of your business's actual health. You might have a flush account after a large mobilization payment, yet remain technically insolvent if those funds are already committed to upcoming labor and material costs. This is why WIP accounting for construction is not just a ledger entry; it's a critical bridge between project management and financial reporting. It ensures that every dollar spent in the field is accurately reflected on your financial statements, providing the structural integrity needed for lender-ready financials and long-term stability. Without this system, you're essentially flying blind, making strategic decisions based on incomplete or misleading data.

The Failure of Traditional Bookkeeping for Contractors

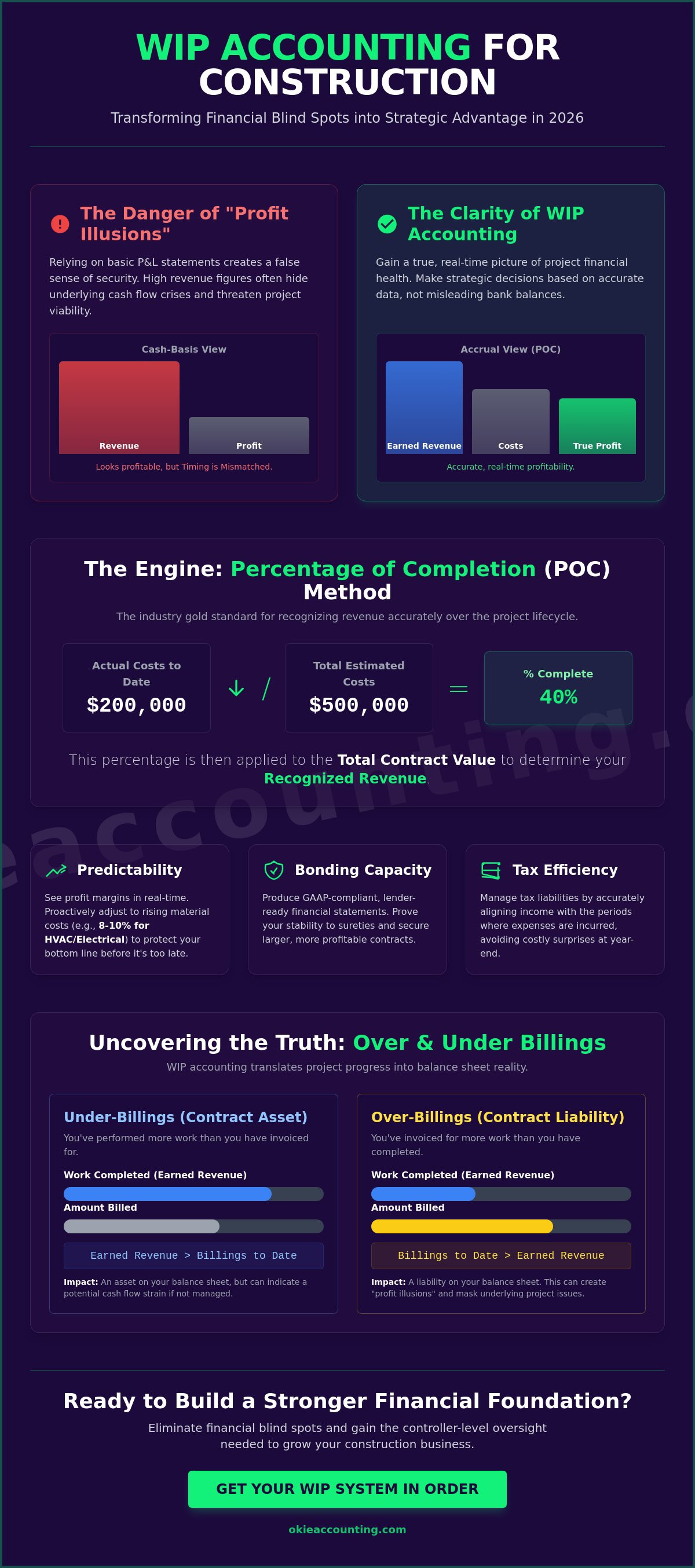

Simple bookkeeping works for retail stores where a sale and the cost of goods happen simultaneously. In construction, the timing of costs and billings rarely aligns. If you rely on basic P&L statements, you'll likely encounter "profit illusions." These occur when you receive a large progress payment that looks like income but actually represents future work you haven't performed yet. Mismatched timing leads to cash flow crises, especially when growing contractors outgrow standard reports. Moving to specialized construction bookkeeping services allows you to track these variances before they drain your reserves. A standard P&L might show you're making money, but it won't tell you if you're borrowing from tomorrow's payroll to pay today's vendors. This lack of visibility is a primary reason why even high-revenue firms fail during economic shifts.

Revenue Recognition and the POC Method

The Percentage of Completion (POC) method is the industry gold standard for revenue recognition. It recognizes revenue based on the actual costs you've incurred relative to your total estimated project costs. The formula is straightforward: (Actual Costs to Date / Total Estimated Costs) = % Complete. This percentage is then applied to the total contract value to determine how much revenue you can legally claim on your financials. This method aligns with GAAP standards and provides a more accurate real-time view than the Completed-contract method, which delays revenue recognition until a project is finished. By using the POC method, you maintain a disciplined, data-driven perspective on your profitability throughout the entire lifecycle of the build.

WIP accounting for construction provides several strategic advantages:

Predictability: You see profit margins as they happen, not months after the fact.

Bonding Capacity: Sureties and lenders demand POC reporting to verify your financial readiness for larger projects.

Tax Efficiency: Accurate recognition helps you manage tax liabilities by aligning income with the periods where expenses are actually incurred.

In a market where material costs for electrical gear and HVAC equipment are rising by 8-10%, having this level of oversight is essential. It allows you to adjust your revised estimates in real-time, protecting your bottom line from the margin compression that often plagues unorganized firms. This transition from basic administration to a foundational system is what distinguishes a surviving business from a thriving strategic partner.

The Anatomy of a WIP Schedule: Essential Components

A WIP schedule is the primary engine for WIP accounting for construction. It isn't a static report; it's a dynamic mechanism that captures the financial pulse of every job in your portfolio. To build a reliable schedule, you must track three core data points with absolute precision: the total contract amount, your total estimated costs, and your actual costs incurred to date. This Guide to Work in Progress (WIP) from the IECI highlights how these components form the bedrock of construction financial management. Without these variables, your reporting remains surface-level and lacks the depth needed for true profit protection.

Direct project costs like labor, materials, and subcontractors are the backbone of the WIP. However, strategic firms also account for allocated overhead. Including a portion of indirect costs, such as insurance or equipment depreciation, provides a more accurate view of true project profitability. The integrity of your WIP depends entirely on the quality of data coming from the field. If your team doesn't code invoices correctly or submit time cards on time, your "Actual Costs" will be perpetually lagged. This delay makes it impossible to catch budget overruns before they erode your margins.

Contract Value and Change Order Management

The "Total Contract Price" in your WIP must be a living number that includes every signed change order. Verbal approvals represent a significant risk to your financial health. If a project manager proceeds with work based on a handshake without updating the WIP schedule, your revenue recognition will be skewed. For unpriced change orders, a conservative approach is best. Recognize the costs as they occur, but wait to recognize the revenue until the price is finalized and signed by the owner. This discipline prevents you from counting profits that may never materialize.

Estimated Costs to Complete: The "Magic Number"

Your WIP is only as reliable as your cost-to-complete estimates. This "magic number" requires project managers to review their budgets monthly and ask: "What will it truly cost to finish this job from today?" Sandbagging estimates to look better in the short term is just as dangerous as over-optimism. Both lead to massive "profit fade" at the end of the project, which can cripple your cash flow and damage your relationship with bonding agents. Establishing a rigorous monthly workflow for these updates ensures your financials remain lender-ready. If your current project tracking feels like guesswork, you might benefit from a professional review of your internal reporting systems.

Interpreting the Data: Over-billing vs. Under-billing

Understanding the numbers on your WIP report is only the first step. To protect your margins, you must learn to interpret what those numbers say about your operational health. WIP accounting for construction centers on two primary conditions: over-billing and under-billing. Over-billing occurs when your billings to date exceed the revenue earned through the percentage of completion method. Conversely, under-billing happens when the work performed surpasses the amount you've actually invoiced. While these appear as simple balance sheet entries, they represent the difference between a project that funds itself and one that drains your corporate reserves.

Lenders and bonding agents look closely at these figures to judge your management capability. Large under-billings often suggest that a contractor is "behind the ball," either due to administrative delays or unresolved disputes with the owner. On the flip side, consistent over-billing is often viewed as a sign of a sophisticated contractor who knows how to manage cash flow. However, this only holds true if the over-billed cash is managed with discipline rather than being spent as found profit. Balancing these two states requires a transition from basic administrative tracking to a strategic financial framework.

The Under-billing Trap: Why Profit Isn’t Cash

Under-billing is essentially an interest-free loan you're providing to your client. When you incur costs for labor and materials but fail to bill for them promptly, you're using your own working capital to fund the project. This creates a significant drag on your construction cash flow management. If your project management team has "slow billing" habits, you'll find yourself in a constant state of financial stress despite having a healthy backlog. Identifying these habits early is vital. Often, under-billing stems from a lack of documentation for change orders or a misunderstanding of the contract's billing milestones. If you aren't billing at the earliest possible moment, you're letting your profit sit in someone else's bank account.

Over-billing: A Strategic Liability

Over-billing is a powerful strategic tool that allows you to fund mobilization and early-stage project costs without relying on lines of credit. It's a proactive way to ensure the project remains cash-flow positive from day one. However, it's vital to remember that over-billed cash is a liability, not profit. It represents money you've collected for work you still owe to the project. Many firms fall into the "job borrowing" cycle, where they use the over-billed cash from a new project to cover the losses or cash gaps of a previous one. This creates a dangerous dependency on new contracts to pay for old mistakes. A fractional controller provides the oversight needed to manage these funds correctly. They ensure you set aside over-billed cash to cover the future costs it was intended for, preventing the house of cards from collapsing when the market shifts.

A Step-by-Step Guide to Implementing WIP Accounting

Moving from a state of financial complexity to one of operational clarity requires a disciplined roadmap. Implementing WIP accounting for construction is not a one-time administrative task; it's the construction of a foundational system that supports every strategic decision you make. This process begins with your Chart of Accounts. You must structure your ledger to support job costing at a granular level, ensuring that direct labor, materials, and equipment costs are assigned to specific projects rather than pooled into general expense categories. Without this structural integrity, your WIP reports will lack the accuracy needed for profit protection.

Once your accounts are clean, establish a rigorous monthly "close" process. This involves reconciling all project data, including subcontractor invoices and field time cards, by a specific deadline. With this data, you can calculate the Percentage of Completion (POC) for every active job using the formula discussed in previous sections. The final accounting step is recording adjusting journal entries. These entries move under-billings to "Contract Assets" and over-billings to "Contract Liabilities" on your balance sheet. This ensures your P&L reflects earned revenue rather than just cash collected, providing a true picture of your financial readiness.

Optimizing Your Software for WIP

Standard QuickBooks is a powerful tool, yet it has significant limitations when it comes to automated POC reporting. Many contractors rely on manual spreadsheets to bridge this gap, which increases the risk of data entry errors and "profit fade." To overcome these hurdles, you can transition from basic bookkeeping to a more integrated approach. Investing in specialized QuickBooks software training for your internal team can help you build workarounds that automate much of the WIP calculation. This shift reduces the administrative burden on your staff and provides leadership with real-time visibility into project margins.

The Monthly WIP Review Meeting

The most critical step in this guide is the monthly WIP review meeting. This isn't just a check-in; it's a strategic oversight session involving project managers, bookkeepers, and owners. The agenda should focus on a project-by-project financial review to identify variances between estimated and actual costs. By comparing the "Revised Estimates" to the work performed, you can spot "profit fade" before it ruins a project's bottom line. This meeting transforms your WIP from a backward-looking report into a proactive early warning system. If you're ready to build a more predictable financial future, schedule a discovery call to discuss your reporting needs.

Scaling Your Firm with Strategic Financial Oversight

Mastering WIP accounting for construction is the definitive turning point where a contractor stops simply reacting to project crises and starts driving long-term business health. While basic bookkeeping records what has already happened, strategic financial oversight uses WIP data to build a blueprint for future stability. This transition allows you to move beyond granular operational details and focus on the broader implications of your financial health. By treating your WIP schedule as a forward-looking early warning system, you gain the clarity needed to navigate a 2026 market characterized by uneven growth and rising material costs.

Accurate WIP data is the fuel for sophisticated Cash Flow Forecasting. It allows you to see exactly when cash will be tied up in under-billings and when over-billed funds must be reserved for upcoming labor and equipment expenses. In an environment where electrical gear and HVAC prices are predicted to rise by 8-10%, this level of visibility is non-negotiable. It ensures that your growth is funded by actual profits rather than temporary cash surpluses. This structured approach creates a sense of order and predictability that mirrors the organized systems necessary for a scaling firm.

Increasing Bonding Capacity and Credibility

Sureties and banks view your WIP schedule as a primary indicator of your management competence. If you seek to secure larger credit lines or bid on substantial public infrastructure projects, "clean" financials are your most valuable asset. A messy or non-existent WIP signals to lenders that you lack control over your project margins, which often results in denied bonds or high-interest rates. For those just starting to build these systems, Mastering QuickBooks for Contractors provides the foundational setup required to produce these lender-ready statements. Establishing this credibility early allows you to compete for the $100 billion data center construction market with confidence.

The Fractional Controller Advantage

There is a clear distinction between basic administrative tasks and high-level strategic leadership. While a bookkeeper records transactions, a controller uses WIP accounting for construction to protect your margins from market volatility and labor shortages. Our fractional controller services provide this specialized oversight without the overhead of a full-time executive. We act as a disciplined mentor, helping you interpret complex data to make informed, proactive choices. This partnership transforms your financial department from a cost center into a strategic engine for growth. If you are ready to eliminate financial blind spots and stabilize your cash flow, we invite you to take the next step toward operational clarity and long-term profit protection.

Building Your Financial Foundation for 2026

Transitioning from reactive bookkeeping to proactive financial leadership is the most significant step you can take to protect your firm's future. By implementing WIP accounting for construction, you move beyond simple administrative tasks and build a structural framework that ensures every project remains profitable. You've learned how to identify the cash flow traps of under-billing and how to use over-billing as a strategic tool for mobilization. These systems don't just organize your data; they provide the lender-ready credibility needed to secure larger bonds and scale your operations with confidence.

At Okie Accounting Group LLC, we provide specialized expertise in construction and real estate accounting to help you navigate these complexities. Our fractional controller services offer nationwide remote financial leadership, allowing you to focus on your builds while we manage your structural integrity. Ready to stop guessing and start growing? Book a Discovery Call with Okie Accounting Group LLC today. We're invested in your success and ready to help you build a more stable, data-driven business.

Frequently Asked Questions

Is WIP accounting required for small construction companies?

WIP accounting is not legally mandated for the smallest cash-basis firms, but it is a functional requirement for any contractor seeking growth or bonding. Once your revenue reaches certain thresholds or you take on long-term contracts, GAAP standards like ASC 606 require you to recognize revenue based on the percentage of completion. Without these reports, you cannot accurately assess your tax liabilities or true profitability.

How often should a construction company run a WIP report?

You should run and review a WIP report at least once per month as part of your standard financial close process. This frequency allows you to catch budget variances and profit fade early enough to take corrective action in the field. Waiting longer than 30 days to reconcile your project data leaves you vulnerable to cash flow gaps that can derail your operations during high-growth periods.

What is the difference between a WIP report and a job cost report?

A job cost report focuses on historical data, showing you exactly what has been spent on labor and materials to date. In contrast, WIP accounting for construction uses those costs to determine your earned revenue, over-billings, and under-billings. While the job cost report helps you manage the field, the WIP report adjusts your balance sheet and P&L to reflect your true financial position.

Can I do WIP accounting in QuickBooks Online?

Yes, you can perform WIP accounting in QuickBooks Online, though the platform does not offer a native, automated WIP module. You must set up a custom Chart of Accounts and use manual journal entries to record contract assets and liabilities at the end of each month. Many firms find that specialized training or controller-level oversight is necessary to ensure these manual workarounds remain accurate and lender-ready.

Why do banks ask for a WIP schedule for construction loans?

Banks demand a WIP schedule because it reveals whether you are "borrowing" from future projects to pay for current ones. They use this report to verify that you have enough remaining contract value and cash to finish all active jobs. A clean WIP schedule demonstrates that you have the disciplined systems in place to manage complex projects without defaulting on your financial obligations.

What is profit fade and how does WIP accounting help prevent it?

Profit fade is the gradual erosion of your gross margin as a project progresses, often caused by underestimated costs or unrecorded change orders. WIP accounting for construction prevents this by requiring a monthly review of revised estimates against actual costs incurred. This disciplined comparison forces project managers to acknowledge budget overruns in real-time, allowing leadership to adjust strategy before the profit disappears entirely.

Is over-billing a good or bad thing for my cash flow?

Over-billing is generally positive for your immediate cash flow because it provides the working capital needed to fund project mobilization without debt. However, it is technically a liability on your balance sheet because you have collected money for work you haven't yet performed. Problems arise only when contractors treat over-billed cash as found profit and spend it on non-project expenses, leading to a cash crunch later.

How do I calculate percentage of completion for a fixed-price contract?

To calculate the percentage of completion, divide your total actual costs incurred to date by your total estimated costs at completion. For example, if you've spent $50,000 on a job estimated to cost $100,000, you are 50% complete. You then multiply this percentage by the total contract price to determine the revenue you should recognize on your current financial statements, regardless of what you've actually billed.

Comments